Compensation Guide

These recommendations are a starting point for finance and pulpit committees as they discuss salary and benefit needs with the pastor. It is our hope that it will be used to help churches make informed decisions regarding the compensation of their pastor.

The Minister’s Program has produced the Guide for our churches and pastors for the last 25 years. We continue to receive positive responses to our efforts and we hope that you will find this tool helpful.

An open and frank discussion about the salary needs of the pastor should not be a difficult or uncomfortable experience for either party. The church has a responsibility to provide a fair and adequate salary for their pastor and the pastor has a responsibility to serve the church faithfully. Paul spoke about this relationship in 1 Corinthians 9:9-14.

The church should review the pastor’s salary on an annual basis. These reviews should be in the form of meetings attended by the church’s finance committee and the pastor with the intent of considering all issues that affect the pastor’s compensation plan.

This is the twenty-fifth year that the Minister’s Program has published the Church’s Guide to Basic Compensation for our churches and pastors. For those of you that regularly refer to this publication, you will note that it has increased in size.

Few topics generate more interest in the local church than minister’s compensation, perhaps because the minister’s salary is often the largest single line item in the church’s budget. Every Christian and each church is called upon to practice responsible stewardship as it relates to the financial matters of the church.

Regardless of the order of worship in a church or the special events that may be planned on Sunday, there is nothing more important that takes place than the reading, teaching, and preaching of God’s Word. With that in mind, each church should consider carefully and compensate fairly the person it appoints to stand before the congregation each week to carry out this important task.

1 Timothy 5:17-18, Paul writes,

“Let the elders that rule well be counted worthy of double honour, especially they who labour in the word and doctrine. For the Scripture sayeth Thou shalt not muzzle the ox that treadeth out the corn. And, The labourer is worthy of his reward.”

Most ministers and churches would agree that pastors are called first by God rather than by the church, and that they are accountable to God for how they lead the church. At the same time, pastors and churches both have expectations from each other as to how they will work together under God’s leadership. Because of these expectations, establishing a regular process for reviewing both compensation and performance are vital to a successful relationship between pastor and church.

When the church and pastor meet to consider matters of compensation, we hope that you will find this guide helpful.

The Minister’s Program has produced the Guide for our churches and pastors for the last 25 years. We continue to receive positive responses to our efforts and we hope that you will find this tool helpful.

An open and frank discussion about the salary needs of the pastor should not be a difficult or uncomfortable experience for either party. The church has a responsibility to provide a fair and adequate salary for their pastor and the pastor has a responsibility to serve the church faithfully. Paul spoke about this relationship in 1 Corinthians 9:9-14.

The church should review the pastor’s salary on an annual basis. These reviews should be in the form of meetings attended by the church’s finance committee and the pastor with the intent of considering all issues that affect the pastor’s compensation plan.

This is the twenty-fifth year that the Minister’s Program has published the Church’s Guide to Basic Compensation for our churches and pastors. For those of you that regularly refer to this publication, you will note that it has increased in size.

Few topics generate more interest in the local church than minister’s compensation, perhaps because the minister’s salary is often the largest single line item in the church’s budget. Every Christian and each church is called upon to practice responsible stewardship as it relates to the financial matters of the church.

Regardless of the order of worship in a church or the special events that may be planned on Sunday, there is nothing more important that takes place than the reading, teaching, and preaching of God’s Word. With that in mind, each church should consider carefully and compensate fairly the person it appoints to stand before the congregation each week to carry out this important task.

1 Timothy 5:17-18, Paul writes,

“Let the elders that rule well be counted worthy of double honour, especially they who labour in the word and doctrine. For the Scripture sayeth Thou shalt not muzzle the ox that treadeth out the corn. And, The labourer is worthy of his reward.”

Most ministers and churches would agree that pastors are called first by God rather than by the church, and that they are accountable to God for how they lead the church. At the same time, pastors and churches both have expectations from each other as to how they will work together under God’s leadership. Because of these expectations, establishing a regular process for reviewing both compensation and performance are vital to a successful relationship between pastor and church.

When the church and pastor meet to consider matters of compensation, we hope that you will find this guide helpful.

WHAT IS THE

CHURCH’S GUIDE TO BASIC COMPENSATION?

CHURCH’S GUIDE TO BASIC COMPENSATION?

In the mid-1980s the Minister’s Program discovered that the average age of the FWB minister was increasing at a rate which would result in widespread shortages of pastors over the next few decades. Anecdotal evidence also indicated that the salary of FWB pastors lagged far behind churches of other denominations who were similar in size and geographic location.

As a result of this information the MP designed and published the “Church’s Guide to Basic Compensation” and it has been made available to the every church within the Convention for 21 years. Originally based on compensation surveys within the Convention, the publication was never intended to establish set rates of pay for pastors but rather to be used as a tool and guide for the discussion of pastoral compensation.

As a result of this information the MP designed and published the “Church’s Guide to Basic Compensation” and it has been made available to the every church within the Convention for 21 years. Originally based on compensation surveys within the Convention, the publication was never intended to establish set rates of pay for pastors but rather to be used as a tool and guide for the discussion of pastoral compensation.

Twenty-Fifth Edition

This guide is based on YOUR CHURCH! It does not use averages from our Convention or other denominations. It uses your budget or annual record of giving and the average attendance as each church may record.

Using the average attendance and budget presents an accurate picture of the church’s ability to meet the compensation suggestions presented in this booklet. Even though a pastor may serve the needs of non-members they cannot be counted on to provide regular support to the church’s ministry and this lack of giving must be taken into consideration.

Employment Status - Bi-vocational and part-time statuses will be taken into consideration. Pastors are considered bi-vocational when the pastor is employed outside of the church. Many of our pastors today are bi-vocational and provide a valuable ministry to churches who cannot afford to pay their pastors a living wage.

Church Staff - Guidance on staff positions such as associate pastors, youth pastors, and ministers of music will also be included in this guide.

Base Income - In the past we have tried to define direct income as the pastor’s base income plus housing, utilities, and FICA. Since housing and utilities can vary so widely they are being left out of the calculation. It is better to allow the pastor to set these numbers and have them accounted for in such a way as to gain the maximum tax benefit available.

FICA - For Social Security and Medicare tax purposes the pastor is defined as a “common law employee.” This designation requires the pastor to pay FICA tax at the rate of a self employed individual, or 15.30%. This is quite a sum and churches are encouraged to pay one half of this amount to lessen the tax burden on their pastor. While the church’s contribution is taxable income, it is still a big help to your pastor.

Professional Assistance - Everyone wants to make certain that the business affairs of the church are conducted in a manner that is above reproach, and it is often advisable to enlist the aid of a qualified tax professional in determining benefits and deductible items.

Benefits - In the past benefits have included retirement, disability, group life, and health insurance. With the complexity of tax consequences increasing, churches are being asked to consider a percentage of the direct income to be used as the pastor directs within IRS guidelines.

Accountable Plans - Every church should reimburse their pastor for mileage, conferences and conventions. Proper reporting by the pastor is necessary to insure that the AP does not become taxable income.

Comparable State and Private Sector

Salaries

Churches often ask what are similar positions to a pastor’s role in the local church? A pastor wears many hats. They are speakers, teachers, life coaches, counselors, advisers, and fill other roles. In addition they are on call 24 hours a day. While there may not be an exact job description in the private or government workplace there are some comparisons.

The Bureau of Labor Statistics reported in May 2016 that in North Carolina post secondary philosophy and religion teachers averaged $77,420, high school teachers earned $45,200, and family and marriage therapists averaged $50,860.

These positions are mentioned for your consideration and can provide some insight into matters regarding compensation.

Using the average attendance and budget presents an accurate picture of the church’s ability to meet the compensation suggestions presented in this booklet. Even though a pastor may serve the needs of non-members they cannot be counted on to provide regular support to the church’s ministry and this lack of giving must be taken into consideration.

Employment Status - Bi-vocational and part-time statuses will be taken into consideration. Pastors are considered bi-vocational when the pastor is employed outside of the church. Many of our pastors today are bi-vocational and provide a valuable ministry to churches who cannot afford to pay their pastors a living wage.

Church Staff - Guidance on staff positions such as associate pastors, youth pastors, and ministers of music will also be included in this guide.

Base Income - In the past we have tried to define direct income as the pastor’s base income plus housing, utilities, and FICA. Since housing and utilities can vary so widely they are being left out of the calculation. It is better to allow the pastor to set these numbers and have them accounted for in such a way as to gain the maximum tax benefit available.

FICA - For Social Security and Medicare tax purposes the pastor is defined as a “common law employee.” This designation requires the pastor to pay FICA tax at the rate of a self employed individual, or 15.30%. This is quite a sum and churches are encouraged to pay one half of this amount to lessen the tax burden on their pastor. While the church’s contribution is taxable income, it is still a big help to your pastor.

Professional Assistance - Everyone wants to make certain that the business affairs of the church are conducted in a manner that is above reproach, and it is often advisable to enlist the aid of a qualified tax professional in determining benefits and deductible items.

Benefits - In the past benefits have included retirement, disability, group life, and health insurance. With the complexity of tax consequences increasing, churches are being asked to consider a percentage of the direct income to be used as the pastor directs within IRS guidelines.

Accountable Plans - Every church should reimburse their pastor for mileage, conferences and conventions. Proper reporting by the pastor is necessary to insure that the AP does not become taxable income.

Comparable State and Private Sector

Salaries

Churches often ask what are similar positions to a pastor’s role in the local church? A pastor wears many hats. They are speakers, teachers, life coaches, counselors, advisers, and fill other roles. In addition they are on call 24 hours a day. While there may not be an exact job description in the private or government workplace there are some comparisons.

The Bureau of Labor Statistics reported in May 2016 that in North Carolina post secondary philosophy and religion teachers averaged $77,420, high school teachers earned $45,200, and family and marriage therapists averaged $50,860.

These positions are mentioned for your consideration and can provide some insight into matters regarding compensation.

Information about the Categories

For a recommendation to be meaningful it must fit the characteristics of the parties involved. For the pastor the major characteristics are full-time or bi-vocational followed closely by education, and experience.

For a church the principal characteristics for determining compensation are size as expressed by their average attendance and total budget.

Church Categories

Church category is determined by the average attendance. Average attendance is the number of people (attendee = adults and children) in attendance on any given Sunday morning service throughout a 12 month period.

For a church the principal characteristics for determining compensation are size as expressed by their average attendance and total budget.

Church Categories

Church category is determined by the average attendance. Average attendance is the number of people (attendee = adults and children) in attendance on any given Sunday morning service throughout a 12 month period.

Average Attendance Category

25-49 I

50-99 II

100 + III

25-49 I

50-99 II

100 + III

A healthy church receives in gifts and offerings anywhere from $20-$30 per attendee per week or annual gifts of $1,040-$1,560. Example: A church with 75 attendees will probably have a budget of $97,500 +/-. (75 x $1,300 = $97,500)

Pastor Categories

There are several considerations for the pastor which include:

This method is not a “one size fits all” approach. All the numbers used for calculating recommendations are based on the church’s average attendance and their budget. The calculations also take into account the pastor’s vocational status, experience and education. All of our congregations and pastors are unique and every situation deserves individual consideration. The information in this guide revolves around two inescapable realities. One, the higher the attendance the more complex a pastor’s role becomes, and two, the size of the budget determines a church’s ability to pay.

Pastor Categories

There are several considerations for the pastor which include:

- Vocational Status: Full time, part time or bi-vocational?

- Experience

- Education

This method is not a “one size fits all” approach. All the numbers used for calculating recommendations are based on the church’s average attendance and their budget. The calculations also take into account the pastor’s vocational status, experience and education. All of our congregations and pastors are unique and every situation deserves individual consideration. The information in this guide revolves around two inescapable realities. One, the higher the attendance the more complex a pastor’s role becomes, and two, the size of the budget determines a church’s ability to pay.

HOW DO YOU USE THIS GUIDE?

The most important thing to remember is that when you apply these guidelines to your church’s individual situation, you have reached a place to start the conversation. This guide is not meant to be the final say in matters relating to your pastor or congregation. This information is a tool that should be modified to help you determine fair and equitable compensation for your pastor. Each church should take into account major factors such as average attendance, the church’s revenue from tithes and offerings, the minister’s education, and experience. You need to adjust these numbers for your situation.

Each of the following headings play a valuable role in the church decision making process and should be considered carefully.

Vocational Status

Category I: Experience has shown that category I churches almost always employ part time or bi-vocational pastors.

Category II: Smaller category II churches may employ bi-vocational or part time pastors while larger churches in this category employ full time pastors.

Category III: These churches almost always employ full time pastors.

Category Factor

Base salaries for pastors can be calculated by using a percentage factor of the budget for each category as follows:

Category I 50% of budget

Category II 40% of budget Full Time

Category II 30% of budget Bi-vocational

Category III 30% of budget

Adjustments

Education

Degree Adjustment

2 Year 0%

4 Year 10%

Masters 13%

Doctorate 15%

Experience

Years Adjustment

0-5 0%

6-9 5%

10-19 10%

20-29 15%

30+ 20%

Benefits

A percentage of the direct income to be used as the pastor directs for retirement, etc. within IRS guidelines.

15%

FICA

The pastor is required to pay FICA tax at the rate of 15.30%. The church should consider paying one half.

Sliding Scale

By using just 3 categories we have attempted to make this process simple. However, the simplicity works best in the middle of the scale and not at either end. At either end of the scale the church should consider sliding the factor up or down as necessary.

An example of this is when a church is at the low or high end of a category they may choose to adjust or slide the percentage up or down to match their situation. For example your church is a category II with an average attendance of 60 and a budget of $60,000. Your pastor is bi-vocational so the category factor is 30% which calls for a base of $18,000. It is appropriate to slide the factor up to 40% or even higher.

Conversely if your church is a category II with an average attendance of 90 and a budget of $150,000 the church may choose to slide the factor down below 40%.

The main point is this: This approach assists the church in determining a starting point for a meaningful discussion about compensation by using calculations that are unique to their particular congregation and pastor.

Each of the following headings play a valuable role in the church decision making process and should be considered carefully.

Vocational Status

Category I: Experience has shown that category I churches almost always employ part time or bi-vocational pastors.

Category II: Smaller category II churches may employ bi-vocational or part time pastors while larger churches in this category employ full time pastors.

Category III: These churches almost always employ full time pastors.

Category Factor

Base salaries for pastors can be calculated by using a percentage factor of the budget for each category as follows:

Category I 50% of budget

Category II 40% of budget Full Time

Category II 30% of budget Bi-vocational

Category III 30% of budget

Adjustments

Education

Degree Adjustment

2 Year 0%

4 Year 10%

Masters 13%

Doctorate 15%

Experience

Years Adjustment

0-5 0%

6-9 5%

10-19 10%

20-29 15%

30+ 20%

Benefits

A percentage of the direct income to be used as the pastor directs for retirement, etc. within IRS guidelines.

15%

FICA

The pastor is required to pay FICA tax at the rate of 15.30%. The church should consider paying one half.

Sliding Scale

By using just 3 categories we have attempted to make this process simple. However, the simplicity works best in the middle of the scale and not at either end. At either end of the scale the church should consider sliding the factor up or down as necessary.

An example of this is when a church is at the low or high end of a category they may choose to adjust or slide the percentage up or down to match their situation. For example your church is a category II with an average attendance of 60 and a budget of $60,000. Your pastor is bi-vocational so the category factor is 30% which calls for a base of $18,000. It is appropriate to slide the factor up to 40% or even higher.

Conversely if your church is a category II with an average attendance of 90 and a budget of $150,000 the church may choose to slide the factor down below 40%.

The main point is this: This approach assists the church in determining a starting point for a meaningful discussion about compensation by using calculations that are unique to their particular congregation and pastor.

{kind=link}

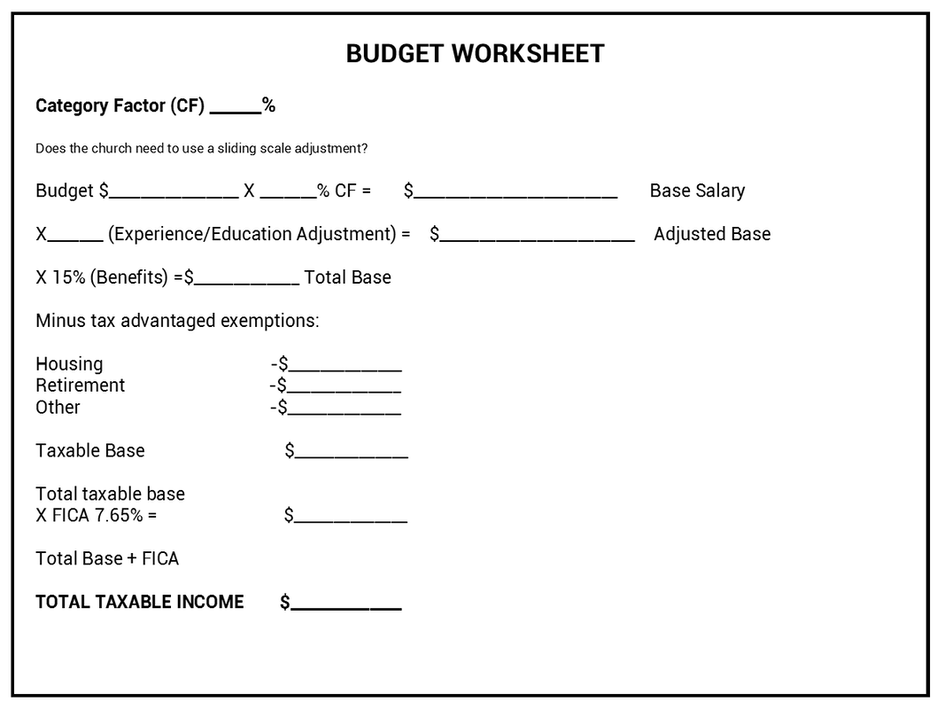

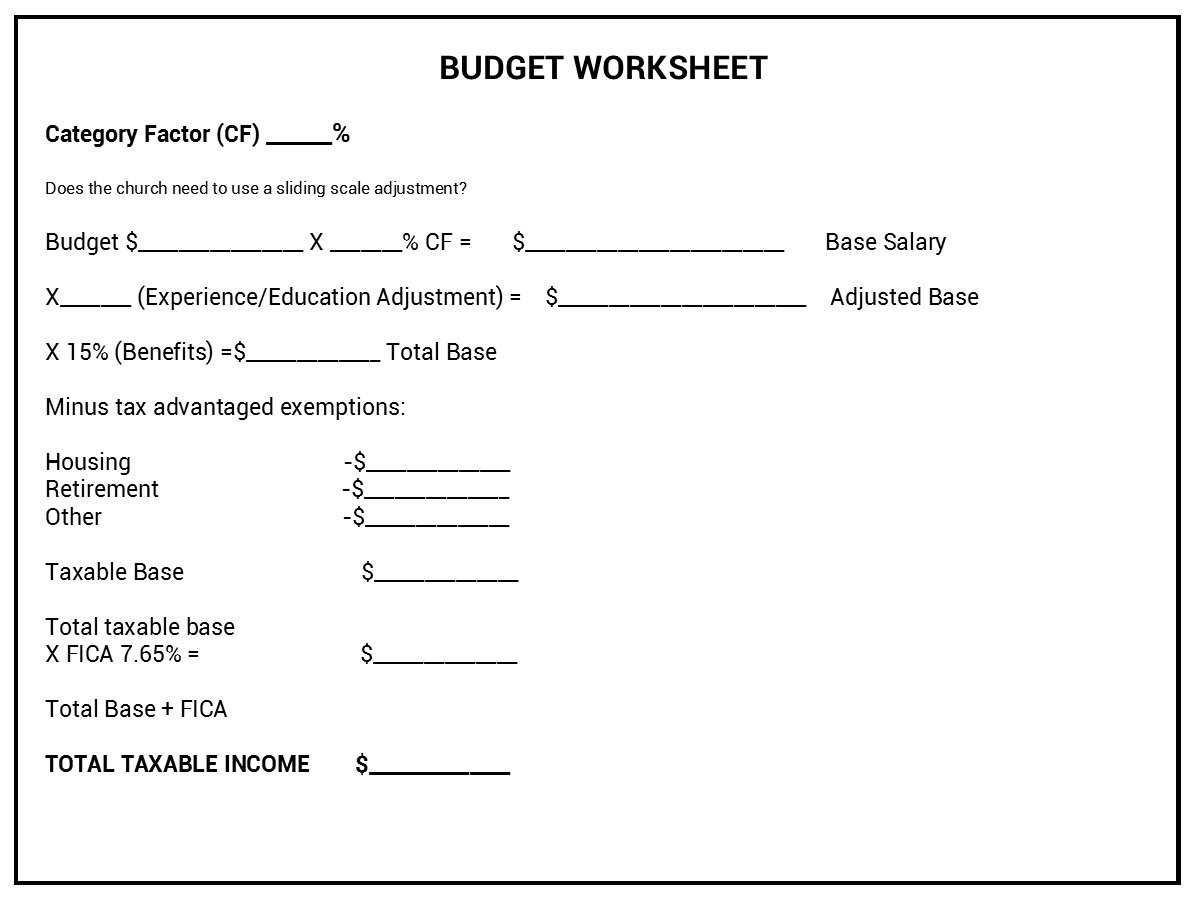

Example:

Your minister has a 4 year degree and 12 years of experience in the pastorate. Your church has an average attendance of 90 people and a budget of $100,000. To use the Church’s Guide to Basic Compensation, find the church category which in this case would be a II and your pastor is full time which indicates a factor of 40% of the budget.

Multiply the budget by the category factor.

$100,000 X 40% = $40,000 Base salary.

Now calculate the experience and education adjustment which is 20% and multiply the base by 1.20 which gives you an adjusted base of $40,000 X 1.20 = $48,000 Total Base

Add 15% benefits to the total base by multiplying the base by 1.15%.

$48,000 X 1.15 = $55,200 Total base

Deduct housing allowance and qualified retired contributions, which in this example will be:

$55,200 Total

- $17,400 Housing

- $ 4,800 Retirement

$33,000 Total taxable base

2,524 FICA 7.65% X $33,000

$35,524 Total taxable income

MINISTRY STAFF

Over the years we have seen our larger churches utilize larger staffs in order to provide a higher level of ministry and care for their congregations. These positions include associate pastors, youth pastors, minister of music, musicians, and others.

Staff pastors range from bi-vocational who work part time to full time positions with a heavy work load. A rule of thumb is that an associate pastor is compensated at 75% +/- of the senior pastor’s base salary.

Regardless of the title associated with a staff position compensation is based upon the job description, amount of time the individual works, experience, and qualifications.

Lastly, when it comes to gender issues every church should adopt the philosophy of equal pay for equal work.

Your minister has a 4 year degree and 12 years of experience in the pastorate. Your church has an average attendance of 90 people and a budget of $100,000. To use the Church’s Guide to Basic Compensation, find the church category which in this case would be a II and your pastor is full time which indicates a factor of 40% of the budget.

Multiply the budget by the category factor.

$100,000 X 40% = $40,000 Base salary.

Now calculate the experience and education adjustment which is 20% and multiply the base by 1.20 which gives you an adjusted base of $40,000 X 1.20 = $48,000 Total Base

Add 15% benefits to the total base by multiplying the base by 1.15%.

$48,000 X 1.15 = $55,200 Total base

Deduct housing allowance and qualified retired contributions, which in this example will be:

$55,200 Total

- $17,400 Housing

- $ 4,800 Retirement

$33,000 Total taxable base

2,524 FICA 7.65% X $33,000

$35,524 Total taxable income

MINISTRY STAFF

Over the years we have seen our larger churches utilize larger staffs in order to provide a higher level of ministry and care for their congregations. These positions include associate pastors, youth pastors, minister of music, musicians, and others.

Staff pastors range from bi-vocational who work part time to full time positions with a heavy work load. A rule of thumb is that an associate pastor is compensated at 75% +/- of the senior pastor’s base salary.

Regardless of the title associated with a staff position compensation is based upon the job description, amount of time the individual works, experience, and qualifications.

Lastly, when it comes to gender issues every church should adopt the philosophy of equal pay for equal work.

OTHER CONSIDERATIONS

In addition to the minister’s regular compensation, there are other matters that the church should consider. They are as follows:

2020 IRS Mileage Rate

For those pastors that have accountable plans and are reimbursed by the church for miles traveled, the IRS has set the mileage: Reimbursement rate at 57.5 cents per mile for 2020.

Vacations

Two weeks with one additional week for each 5 years of experience is suggested. The church should budget for the supply speaker.

Christmas Gift

The church should consider a minimum of one week’s salary as an added bonus during the Christmas season.

Sick Leave/Disability

You should agree in writing what the policy of the church will be in the event of sickness or disability. This is especially true in the event that the pastor lives in the parsonage. How long will the parsonage be available and compensation continue? In the event of a total disability the church should continue the pastor’s salary for a minimum of ninety days and up to one hundred and eighty days if possible.

Death Benefits

What does a church do when their present pastor dies? This doesn’t happen very often but when it does, it presents some very difficult choices for the church, especially if a parsonage is involved. These decisions are much easier when the church has considered this possibility beforehand.

While the church has lost their pastor, it is important to consider that the widow has lost her husband, his salary and, in the case of a parsonage, her home. The Minister’s Program recommends that the church continue to pay the widow 70% of the pastor’s salary for a period of 90 days and that she be granted the right of occupying the parsonage for that period of time.

Supply Speakers

When someone is called to fill a pulpit for a service, the church should consider a minimum of $150 per service and mileage at the IRS rate for a round trip from his home. The mileage rate for 2020 is 57.5 cents per mile.

Interim Pastors

If this individual is expected to provide all the pastoral services expected of a regular pastor, then you should use the Church’s Guide to Basic Compensation. Depending on the expectations of the interim pastor, the church and pastor may agree to a percentage of the total recommendations.

Evangelists

The recommended amount is $150 per service with an allowance for mileage and meals if travel will be during meal time. Overnight accommodations, if needed, should be at an acceptable motel at the expense of the church.

2020 IRS Mileage Rate

For those pastors that have accountable plans and are reimbursed by the church for miles traveled, the IRS has set the mileage: Reimbursement rate at 57.5 cents per mile for 2020.

Vacations

Two weeks with one additional week for each 5 years of experience is suggested. The church should budget for the supply speaker.

Christmas Gift

The church should consider a minimum of one week’s salary as an added bonus during the Christmas season.

Sick Leave/Disability

You should agree in writing what the policy of the church will be in the event of sickness or disability. This is especially true in the event that the pastor lives in the parsonage. How long will the parsonage be available and compensation continue? In the event of a total disability the church should continue the pastor’s salary for a minimum of ninety days and up to one hundred and eighty days if possible.

Death Benefits

What does a church do when their present pastor dies? This doesn’t happen very often but when it does, it presents some very difficult choices for the church, especially if a parsonage is involved. These decisions are much easier when the church has considered this possibility beforehand.

While the church has lost their pastor, it is important to consider that the widow has lost her husband, his salary and, in the case of a parsonage, her home. The Minister’s Program recommends that the church continue to pay the widow 70% of the pastor’s salary for a period of 90 days and that she be granted the right of occupying the parsonage for that period of time.

Supply Speakers

When someone is called to fill a pulpit for a service, the church should consider a minimum of $150 per service and mileage at the IRS rate for a round trip from his home. The mileage rate for 2020 is 57.5 cents per mile.

Interim Pastors

If this individual is expected to provide all the pastoral services expected of a regular pastor, then you should use the Church’s Guide to Basic Compensation. Depending on the expectations of the interim pastor, the church and pastor may agree to a percentage of the total recommendations.

Evangelists

The recommended amount is $150 per service with an allowance for mileage and meals if travel will be during meal time. Overnight accommodations, if needed, should be at an acceptable motel at the expense of the church.

Healthcare under the Affordable Care Act (ACA)

The changes that have taken place since the implementation of the ACA are beyond the scope of this publication. Navigating the rules associated with the new law will require the expertise of a professional.

The Minister’s Program is not qualified to provide tax or legal advice so it is imperative that the pastor seek the advice of a qualified tax and insurance adviser.

Publication Resources

For this edition of the “Church’s Guide,” we are using a combination of existing data and information from outside the Convention - resources such as the Bureau of Labor and Statistics along with compensation studies of pastors and staff from www.ThomRainer.com.

The Minister’s Program is not qualified to provide tax or legal advice so it is imperative that the pastor seek the advice of a qualified tax and insurance adviser.

Publication Resources

For this edition of the “Church’s Guide,” we are using a combination of existing data and information from outside the Convention - resources such as the Bureau of Labor and Statistics along with compensation studies of pastors and staff from www.ThomRainer.com.